How to get in touch with your connected consumers. Stuart Ganis of marketing and management software provider ITC joins us on the podcast this week to highlight why it is important for independent insurance agents to stay connected and meet their customers where they want to be met. Stuart makes sure to point out that it’s not too late to get on the technology bandwagon.

Click the picture to go to ITC’s website.

Edwin K. Morris (16s):

Welcome to the trusted advisor podcast brought to you by Iroquois group. Iroquois is your trusted advisor in all things insurance. I am Edwin K. Morris. This week’s guest is stuart Ganis. He is the SVP of sales and business development at Insurance Technologies Corporation. stuart started his career as an insurance producer right out of high school. Eventually he launched a startup agency based in Southern California with his wife, Mary. After the sale of their agencies, Stuart launched a boutique consulting firm, focused on helping independent agencies grow and thrive. As a 30 year veteran in the industry, stuart has consulted more than 700 independent agencies and trained thousands of CEOs, principals, producers, and CSRs.

Edwin K. Morris (1m 2s):

Welcome, stuart. How would you define a connected consumer?

Stuart Ganis (1m 8s):

Nowadays, it’s all of us really. When you think about it, you know, we’re all connected to these devices, unfortunately, in our pockets. So you can go to any restaurant and see a family not looking at one another at the dinner table because we’re too connected. And I would really define it in our industry is people that need immediate gratification. You know, our industry is, has been traditionally used to the phone ringing, us answering the phone, taking some information from somebody, calling them back later, getting them some quotes. Maybe they come into the office and sit at our desk. We chat with them. We get to know them as people. Where nowadays, clients don’t want to do that. Now people want to go to their phone, click a button, fill out a form and see a quote.

Stuart Ganis (1m 48s):

They do not want to go through that entire process. So the connected consumer is really all of us now, including, you know, the, the, the older people, the over sixties, the seventies, I mean, they’re on these social media platforms. They have telephone, they’re in browsers. So the connected consumer is people that, people that demand speed and want things done efficiently and quickly, and don’t want to waste time and sit in your office and do all the things we were doing 25, 30 years ago in this business.

Edwin K. Morris (2m 14s):

So it’s almost the connected consumer could be transferable to the idea of you’re connected to the product, not the people. As I heard you saying about the new behavior anticipation of “just tell me what I need to know”. I don’t, I don’t need to hear about your, your shoes you just bought. So it’s more about connecting to action or connecting to the product. Really. I, it really short changes the whole sales in the traditional mentality of what sales is.

Stuart Ganis (2m 44s):

Yeah. You know, that’s a good point, actually. I, I that’s, that’s a very interesting viewpoint yet. It is connected to the, to the product, you know, on the flip side, there are parts of insurance or certain clientele, or maybe it’s a certain, certain business. Maybe it’s, maybe it’s the client with multiple personal lines policies or the commercial policy that the B2B that still depends on that relationship. They still want the relationship, but they want to do it digitally. They don’t want to do it like we did it 20, 30 years ago, where again, they’re in the office, they’re on the phone all the time. Every time they need something, they have to pick up the phone. They want to send an email or text them. So it’s a blend maybe.

Edwin K. Morris (3m 22s):

That capsule of how things were done. This is not the only industry that has transformed. I think banking is leading that also, is that the mentality of what people expected. You know, I can remember, Oh God, it’s Friday. My, my folks had a small business. We got to go to the bank, got to go, you know? And that was like a big thing. The change in behavior. How does that affect the difference between direct sellers and independent agencies?

Stuart Ganis (3m 48s):

So, you know, the direct sellers have better tools, I believe, where a client could go online, do everything they need to do and never talk to anyone. And quite frankly, that direct seller probably doesn’t want you to, because when you do call in, you’re talking to the, someone in the call center that isn’t as trained as an independent agent, where the independent agent probably lacks a little on the technology side. But if you call them, you’re going to get great information. So you’ve got to figure out how to, if you could mold the two together, somehow I think you have the perfect agent. So independent agents just need to figure out how can I communicate with this client the way they want to communicate, not the way I want to communicate?

Edwin K. Morris (4m 24s):

Which is on a 24-seven availability to an answer, not “I’ll call you back tomorrow when I’m back in the office”.

Stuart Ganis (4m 32s):

Correct. Absolutely. They want, they want an answer. They want a status. They want to know. I mean, listen, you could look up your bank balance. You could look up what to, where you’re sitting for a concert or an event. You can look up pretty much any, your mortgage rate. You could look up your balance for anything. Why is insurance different? Because it’s independent agents don’t want it to be, no, it doesn’t work that way. Unfortunately, it doesn’t work that way.

Edwin K. Morris (4m 54s):

What’s the biggest stumbling block to get there. What do you see as the hurdle that agents have?

Stuart Ganis (5m 0s):

Yeah, so, you know, when I first started the business, it was 1989 and I didn’t have a computer on my desk, which is kind of cool. I’m probably one of the last generations to ever start a job without a computer on their desk. And I’m only 26, isn’t that amazing.

Edwin K. Morris (5m 15s):

Unbelievable, actually.

Stuart Ganis (5m 16s):

I know, I know I look young, but you know, we’re not going to talk about that, but you know what I figured out, you know, I think what happened is these agents, insurance has always been slow to adopt. Okay. When I started our first agency, my wife and I started an agency in 2000, paperless was cutting edge where you would look at banking or mortgage, and they’ve been paperless for five, 10 years. We’ve always been slow to adopt. And then, and then we sold our agency, and around 2009 or 10, when we really, really dug into the internet, it was so odd to do a search and see the companies you sold, competing against you. So now you’ve got carriers that you sell for, selling against you.

Stuart Ganis (5m 59s):

They’re clients that buy direct get this technology, but you don’t. So it’s very difficult. The carriers and the agents need to come together and say, Hey, listen, how do we do this together to where we can still be effective distribution and the client isn’t tempted to go click on your commercial or your link or your pop-up and buy directly from you and cut us out. Because we do offer a lot. Listen, independent agents, we’re not going to go with travel agencies. We’re not going away. We’re here to stay. We are a strong industry. There’s going to be less of us in 10, 15, 20 years, which quite frankly, there should be. The carriers need to give, provide agents with the technology. So clients can look up those statuses. And it’s still branded to the agency because you ask nine out of 10 clients who are with an independent agent who they’re insured with.

Stuart Ganis (6m 41s):

They’re going to say the carrier name. They’re not going to say the insurance, Oh I’m with Stuart Ganis insurance. They’re going to say I’m with travelers insurance. They’re not going to say Stuart Ganis insurance. So they’ve got to figure out how to work together and make that happen and provide technology to agents. And quite frankly, agents hate to use the term, but agents, wet the bed 15, 20 years ago, I think they thought the internet was going to be, you know, like corteroids, you know, Hey, this isn’t going to last, you know? And, and the carriers were like, they were in board meetings, meeting together saying, we need a direct distribution channel because this is the internet. And it’s going to be huge for us. And, you know, the agent blew it quite frankly. I mean, we did, we, we did not do a very good job of embracing social, Google, search. There’s really no dominant independent agency out there, like a Geico or a Progressive or esurance or any of this.

Stuart Ganis (7m 28s):

Yes.

Edwin K. Morris (7m 28s):

All of those other names you just threw out there was born out of not just necessity, but keeping up with the expectation of the consumer, how the interface works.

Stuart Ganis (7m 39s):

Exactly. You’re exactly right. They said the consumer wants something. Agents want to know. People don’t want, they want the relationship. I’ll never devalue the relationship between an independent agent of the client. But my daughter is 20 and she’ll never step foot in an insurance agent’s office. She may never talk to an insurance agent unless she has a claim or a law. She wants to do it on our live phones. They would want to get a quote, buy insurance, do whatever they have to do. It’s not going to happen for this younger generation. They’re not going to do it. So agencies need to adapt to that, look what COVID did. All of a sudden agents are talking about having staff at home. We could have done this 10 years ago.

Edwin K. Morris (8m 13s):

Well, I think a lot of industries are in that same boat of realization that the technology will reduce your overall cost of an organization. If you don’t have to house all these people to work, it’s just going to be a huge change. So what is the relationship, do you see, to this type of customer? How do you keep that relationship?

Stuart Ganis (8m 36s):

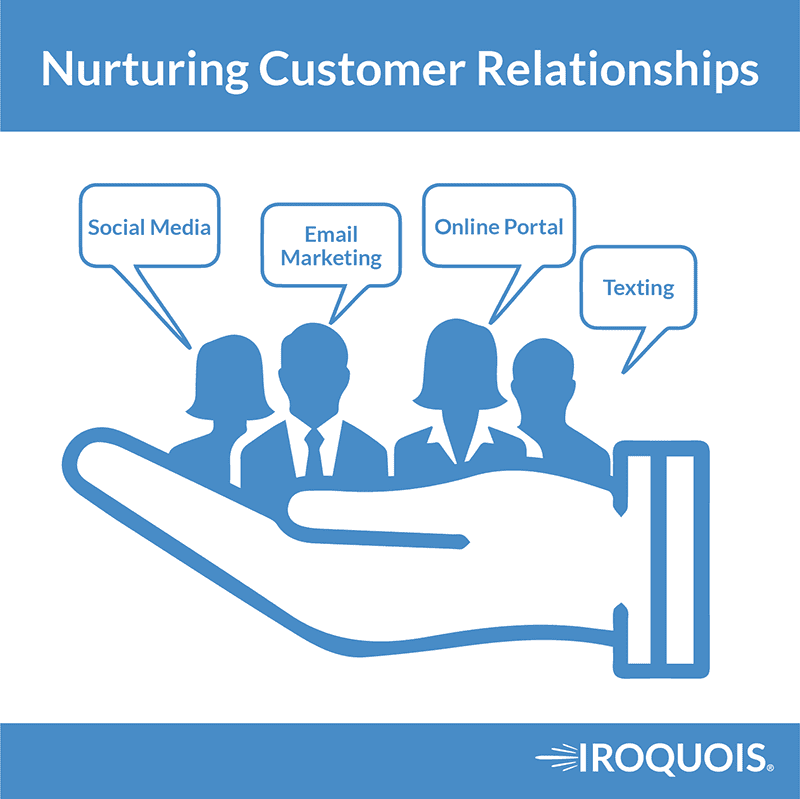

Yeah. So it’s, they’ve got to see you digitally. The, I think it’s the little things. It’s the blocking and tackling it’s, it’s hitting their inbox seven, eight, nine times a year with, with whether it’s a holiday email, a newsletter, or how you doing, a checkup. It’s social media, looking lived in on your social media. I mean, look, if I had an independent agent or any service for that matter, if someone refers me, accountant and attorney any professional, and I went to their Facebook page and they had nine, nine followers and there hasn’t been a post since 2014, they’re off the menu, you’re off the menu. Next. The dream is dead. So, you know, so you’ve got to do the blocking and tackling. You’ve got to have a presence on social. You’ve got to have a presence in their email marketing. You’ve got to text them once in awhile.

Stuart Ganis (9m 17s):

And you’ve got to allow them to communicate with you the way they want to, not the way you want to communicate with them. And that’s where agents have a really hard time, that barrier, where someone will text you a question and you want to call them back. No, text them back! That’s what they want. You know, that’s why they reached out to you. Stick with the form, the original form of communication. So I think it’s really in how you communicate what you do. And, and obviously the basics, a lot of the traditional stuff we’ve always done still stands. You’ve got to cross sell. You’ve got to advise on coverage. You know, my parents had every year, there was a state farm calendar on our magnet, on our refrigerator every single year, they got this calendar from the State Farm agent. So what is that digitally, what does that look like?

Stuart Ganis (9m 59s):

How do we send some, that state farm calendar from the seventies? What is that today? Figure it out and send it to your clients.

Edwin K. Morris (10m 7s):

Well, a lot of that transfers into the customer interface, right? Having a portal, having a on demand access to whatever that is versus the static calendar or the remember, remember the desk calendar that everybody would be giving away, you know, to put on your desk. It’s like, haven’t seen those in a while. How does this all change? We’ve talked about the consumer, but how do you change the mentality of those who have to keep up with what’s happening, with that expectation?

Stuart Ganis (10m 38s):

Yeah. I remember my cousins.. The two youth. You gotta bring some young people in the agency. Seriously, you gotta let the little, you gotta let the young people in the tent and listen to them and let them, you know, it’s amazing when you hire. People complain about millennials, but you hire somebody in their mid twenties and you show them your CRM or your technology. There, wasn’t through within three minutes, they were like “Oh my God, this is so old. You still use this. Oh my God. You know, I have to, I have to double-click”. Yeah. I mean, it’s, it’s unbelievable. They use voice. It’s unbelievable. So you’ve really, you’ve got to, you’ve got to let the young people in the industry, that’s been a problem in this industry forever. You know, we’re still in the mahogany desks and the shag carpet in this business. I mean, let’s, let’s start using Macs for crying out loud, you know? So I think you’ve got to let the young people in and, and look at their behavior and let them, let them provide some solutions.

Edwin K. Morris (11m 25s):

I’ve had to interface with insurance companies. And I’ve noticed that now I’m the claim agent, because I have to take pictures and describe. So I’m like, wow, they’ve, they’ve got this all figured out.

Stuart Ganis (11m 35s):

They really do. It is really something. And you’re right. What you said earlier about communicating. If it’s Friday at 10:00 PM, I should not have to wait until Monday to get an ID card from my insurance agent. That is unacceptable, quite frankly. So either you have a portal on your management system, which most have available. I know we do it IDC, or you have them with a carrier that they could log into the carrier interface and print that ID card. But I remember back in the day, you know, we would work Saturdays and we would stay till two, three, four o’clock because by two, three o’clock, someone was sitting in the dealership and needed insurance to buy a car. And you sold that policy on a Saturday afternoon, where today that agent, agents, aren’t probably getting that call. They’re going online. And if you’re not on that Google or your social, or they haven’t seen you, they’re going direct.

Stuart Ganis (12m 22s):

You’re off the menu.

Edwin K. Morris (12m 23s):

It’s a wholly different expectation on the consumer side because you’re right. I could buy a car in a town I’m not familiar with, but you can just quickly search and find. It’s a self guided methodology versus 40 years ago when the phone book was the biggest indicator of what’s going on. Yeah.

Stuart Ganis (12m 41s):

And now the phone book is so thin it doesn’t even hold doors open anymore. Remember how big that thing was? I used that for every, that was like, you know, that was a booster seat, the door, I mean, it was everything but like, it’s like a magazine now, not much. It’s really bad, it’s kind of crazy, man. But at the same time, look, we could do this. We’ve been through like the nineties, the captains were going to take us out. They pass Gramm-Leach-Bliley in the late nineties, the banks were going to take us out. What happened? Banks started buying agencies and paying more money than we ever imagined. In the early two thousands. The internet was going to take us out. 2010. This has got, we had survived so much as independent agents and we could come out so much stronger if we just apply ourselves to serving the consumer the way they want to be served and you know, and using technology to guide that process.

Edwin K. Morris (13m 34s):

To wrap things up, final question, where is the biggest challenge five years from now?

Stuart Ganis (13m 44s):

I haven’t been figured out this year. No, it’s more of the same. It’s probably what we’re dealing with now on steroids, right? It’s what we’re dealing with now, but it’s on steroids. It’s even that much greater where you know the car company. I mean, Tesla has an insurance company. You’ve got car manufacturers thinking they’re going to get into the insurance business. So you, again, it’s just, you’ve got to go even deeper and deeper. That’s why, if you haven’t started yet, the best time to do email marketing was starting 10 years ago. The other best time is today. So all of this stuff is just, I think it’s what it is now. Just multiply it over time in five years and people, we’re going to have a people shortage in this business. We need to bring young people in and we need to make insurance sexy. Insurance is not sexy. It’s a great industry. I mean, it’s been so good to me. I mean, I’m a high school dropout.

Stuart Ganis (14m 25s):

I should have been the statistic at one time in my life. And I started in the business at 19. Sales manager took me under his wing. And here I am, you know, 30 years later on the podcast with you. So it is a wonderful industry and we’ve got to bring young people in and, and make it, just make it sexier and technology can make it sexier.

Edwin K. Morris (14m 44s):

Well thank you for all of that great conversation. It’s been a joy.

Stuart Ganis (14m 48s):

Thank you so much for having me.

Edwin K. Morris (14m 51s):

Thanks for listening to this edition of the trusted advisor podcast brought you by Iroquois group. Iroquois, your trusted advisor for all things, insurance, and remember get out of the office and sell. This program was recorded Live at the Cohen multimedia studio on the grounds of Chautauqua institution. I am Edwin K. Morris, and I invite you to join me for the next edition of the trusted advisor podcast.