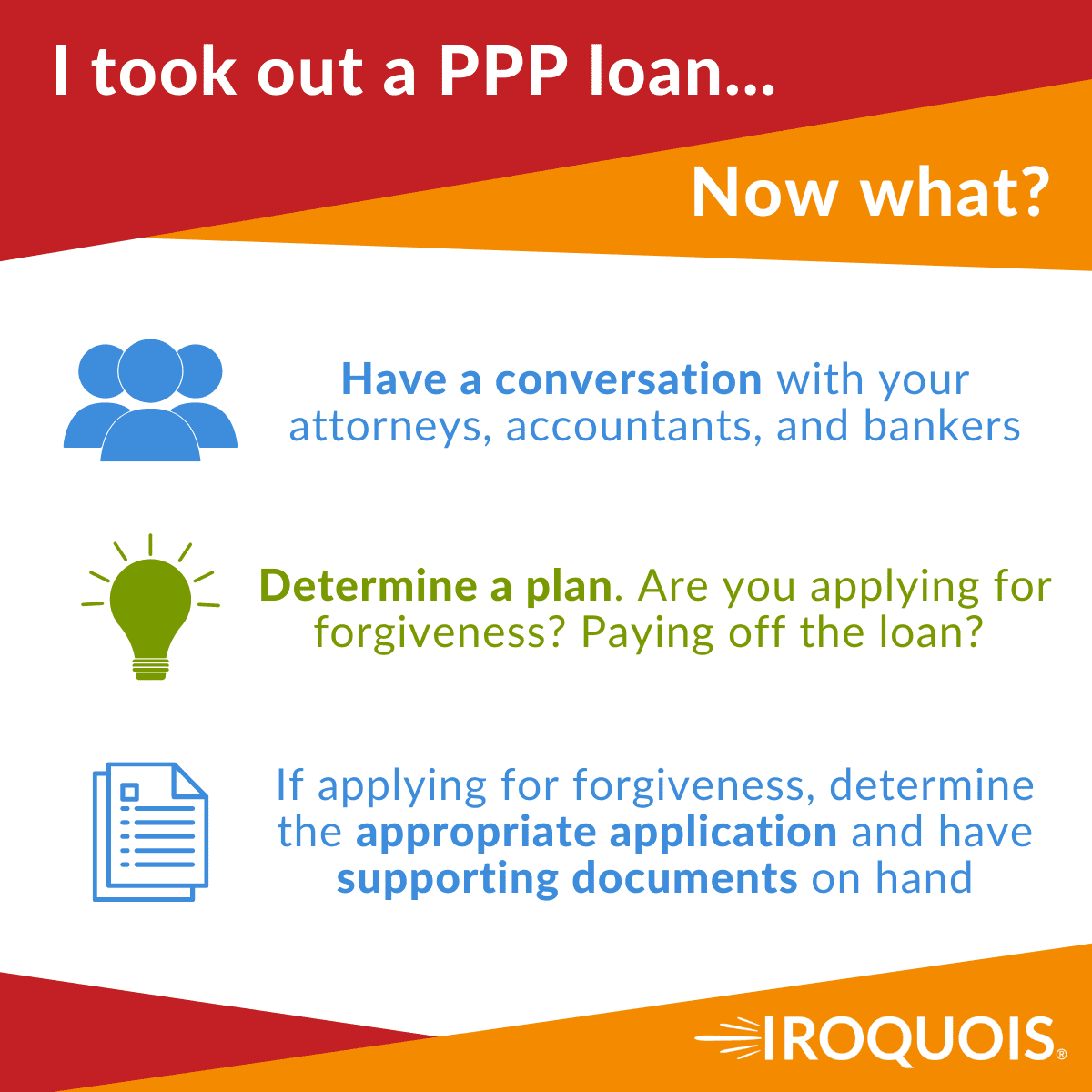

So, you took out a PPP loan – now what? In the second episode of Charlie’s Corner featuring Jenny Shtipelman of National Capital Bank, we cover what’s next for business owners. Whether you are looking to apply for full loan forgiveness or just partial, this episode provides guidance as to what you need ready before you start the process. Listen to part one here.

Don’t forget to visit these important resources.

Don’t forget to visit these important resources.

SBA:

Treasury:

Edwin K. Morris (4s):

Welcome to the trusted adviser podcast brought to you by Iroquois Group. Iroquois is your trusted advisor in all things insurance. This week, you are listening to the special segment of Charlie’s corner hosted by our very own Charlie Venus.

Charlie Venus (21s):

Welcome back to Jenny Shtipelman of National Capital Bank. She joins us again this week to round out our conversation on PPP Loan Forgiveness. Like I had a lot of friends that got the PPP Loan and not knowing how their business was going to be impacted, so if there wasn’t any significant impact to their business, what’s the recommendation for those people in terms of applying for the loan forgiveness?

Jenny Shtipelman (47s):

It could be a controversial conversation, right? And it can be very individual conversation. But so when applying for the original PPP loans and the second PPP loans, some of the certifications that the borrowers had to make were uncertainty, no one knew what was going to happen. I mean, heck the majority of us thought that we were just shutting down for what, six weeks, something like that. And it was all going to be, you know, said and done relatively quickly. And even given that, there was a huge panic. What came to a, a real head is that a lot of businesses realized that they don’t have cash reserves to pay their employees for six weeks without generating any revenue, especially a lot of retail businesses and stuff like that.

Jenny Shtipelman (1m 35s):

For people whose businesses weren’t really impacted, it doesn’t change the fact that at the time that they applied there was uncertainty. And it’s a conversation with them that between them and their attorneys, their accountants, their bankers whether they should apply for forgiveness, or just pay it back. Now, mind you, if you’re just paying it off at this point, you’re going to be responsible now not to just give the money back, but also accrued interest. It’s accruing at 1%. So, you know, not a huge amount. However, you know, depending on the loan amount, it’s some money nonetheless. So it’s an individual decision of how they choose to proceed

Charlie Venus (2m 11s):

Because the impact for a lot of companies was that nobody realized that they would be able to go out and start working remotely and not see a significant impact in their business. Right? People got the money and there wasn’t really the dramatic impact that they thought there was going to be.

Jenny Shtipelman (2m 27s):

It’s up to them. And it may be other impacts that they may consider and it, it, it should be an internal conversation. From our perspective, the bankers perspective, we are not here to advise you whether you should or should not apply for forgiveness. What we’re doing is if you choose not to, then we can tell you how much you owe and what the process is. If you choose to apply for partial forgiveness, we will process and make sure that application is correct based on the bank policies and submit it to the SBA, and then figure out how you can pay off, find the rest of it. Or if you just applied for forgiveness, we just, again, check the application and make sure all the calculations and the documents are in order.

Jenny Shtipelman (3m 8s):

And we submit it. It’s a business decision for every individual borrower.

Charlie Venus (3m 13s):

Now you mentioned earlier that the original loan forgiveness application was 11 pages, right? Is it much simpler now? And what documentation do we need for the loan forgiveness?

Jenny Shtipelman (3m 23s):

So here’s how it’s changed so far. And honestly, I don’t know, some people are asking whether it’s going to change further and TBD. Again, the only thing with this program that is constant is the fact that it keeps changing. So now on the forgiveness side, there’s three different applications and they’re applicable to different types of businesses. Any loan under $150,000, the original PPP Loan, where borrowers have not decreased salaries by more than 25% or decreased staff, can apply using the Simple Application. That is literally a one-pager. The supporting documents, and again, this is all based on the bank policy, So don’t quote me to your bankers on this because it, they may require a different things.

Jenny Shtipelman (4m 10s):

The SBA specifically with a simple application for forgiveness does not require you to submit to them documents proving that you spent money in a certain way, unless it’s the second draw location, then you were required to submit evidence that the revenues went down. So P and L’s or something like that, tax returns. And this is what we advise our borrowers to do is definitely keep a file of something right at your fingertips with all the supporting documents. So if you have employees, your 941s, any type of payroll provider records or anything that shows how you spend the funds. Copies of leases if you paid rent, canceled checks for if it’s insurance or 401k contributions, stuff like that.

Jenny Shtipelman (4m 54s):

’cause what happens is by law, the SBA has to review a certain random number of applications. So it doesn’t matter the size of the loan, all loans over 2 million will be reviewed. And that’s also the law, anything in between that may be randomly selected for a review and once it is that’s where the SBA requests copies of everything to be sent to them. So they can just take a look and confirm how the funds were spent. Most of the time they want third party supporting documents. That’s what, hence the 941s, the payroll provider records, copies of tax returns, things that are actually filed with federal agencies or state agencies, just to show proof, keep the supporting documents at your fingertips, even, you know, whether they’re required or not.

Jenny Shtipelman (5m 40s):

Because if you need to submit it for a review, if you have to submit everything to the SBA within, I believe it’s 15 days, in order to not get a little bit of a red flag.

Charlie Venus (5m 50s):

The only things that can prevent business from qualifying for a forgiveness is if they don’t meet those rules in terms of at least 60% going to payroll and maintaining their staff and at least 75% of the payroll, correct?

Jenny Shtipelman (6m 6s):

Right. And so the Simple Application was number one. Number two is the Easy Application. So anything above a, a 150,000 and up to the limit can be, as long as payroll was not, per employee, was not cut by more than 25%. And if staff wasn’t cut, they qualify for the easy version of the application. And if they have not, and for actually any business that is, that has the loans over $2 million, we recommend that they complete the long-form application. There’s a lot of calculations and we recommend that you get your CPA involved and those things, and et cetera, et cetera, as long as you did everything that you were supposed to do, it doesn’t matter which forgiveness application you complete.

Jenny Shtipelman (6m 49s):

But as long as you have all of the supporting documents then you should be okay.

Charlie Venus (6m 55s):

And once the business owner submits this to their lending institution, I know that you can only speak for yourself on this, but what would typically be the turnaround time to get it to the SBA and then for the SBA to give a thumbs up or thumbs down on the approval?

Jenny Shtipelman (7m 14s):

That all depends. We’ve, we’ve had some back and forth with some of our borrowers. So essentially, and I can speak to the way that the process works in National Capital Bank, is, is that we use a software provider for our forgiveness applications. From the time a borrower receives a link to the portal where they can complete their forgiveness application, they can complete, they can select the type of forgiveness application they want to use, they can upload all the supporting documents in there. Once they click complete and submit to us, that doesn’t mean that they have a completed application. That means that the draft of what they created and completed comes to the bank for review. Then our team goes through the application to make sure that it’s correct, it’s complete and all the required supporting documents for that application type are there.

Jenny Shtipelman (8m 3s):

And that the information actually backs up to the numbers that they’ve completed. And sometimes it is all correct, and sometimes it’s not. And so there’s maybe a little bit of a back and forth in that stage. Then once everything is actually completed and we the bank approve their forgiveness application on our end, we then send an electronic version of the actual forgiveness application to the borrower for the electronic signature. Once we have their signature, it’s considered a completed application. Per the law, the bank has 60 days to between the time that they have a completed application to the time they submit it to the SBA.

Jenny Shtipelman (8m 45s):

Obviously we kind of front load those 60 days to the draft piece because again, we want to make sure that we have as much cushion as possible. And so most of the time when we have a completed application, it goes to the SBA within a matter of days, then we are at the mercy of the SBA. Now I have to say that since the second round of origination, the actual PPP application has finished and they finished with a review. So they’re not busy with origination of the PPP applications, so that finished at the end of June, they have been much, much quicker with turning around forgiveness applications that we submit to them. So by law, the SBA has up to 90 days to respond to the forgiveness application,

Charlie Venus (9m 30s):

If they deny the forgiveness application, then is there an appeal process?

Jenny Shtipelman (9m 34s):

Yes. There is an appeal process. It is outlined in the interim final rule. Knock on wood, I have not had that experience yet.

Charlie Venus (9m 44s):

So do you know what your success rate was thus far?

Jenny Shtipelman (9m 47s):

Or we, we, we have not had the, well, I mean, I guess so far – and Charlie, if you’re jinxing me, we are going to have a separate side conversation.

Charlie Venus (9m 55s):

I promise I’m not!

Jenny Shtipelman (9m 56s):

Exactly, but so far all of the forgiveness applications that we have submitted, except for there’s several that are still being reviewed by the SBA. The SBA has agreed with our assessment of what the forgiveness amount should be, so they’ve approved at, at that amount.

Charlie Venus (10m 13s):

What are you seeing in terms of percentage of forgiveness, 50%, 70%, a hundred percent?

Jenny Shtipelman (10m 16s):

Do you mean what people are applying for amounts of that loan forgiveness?

Charlie Venus (10m 19s):

Yeah.

Jenny Shtipelman (10m 19s):

You, you know what, the majority are actually applying for full forgiveness. There’s some partial ones. It, again, that’s not our decision. Well, it could be our decision if things are just not adding up and then we can potentially apply or approve them for partial forgiveness. We at national capital bank, and granted we’re a small community bank so we’re able to potentially give it a little bit more of a human review and personal touch ’cause just our a volume of applications is, is probably much less than that of Bank of America or large behemoths where they have probably thousands if not millions of applications, and the SBA has I think that the total application number was over 7 million.

Jenny Shtipelman (11m 2s):

It was just a lot of PPP applications. We will probably work that out, whether the borrower’s going to apply for full forgiveness, or if they’re, if we disagree on the number, then they’re not going to apply for full forgiveness and then we’re going to fully approve them. So it’s not like they’re applying for full forgiveness and I say, no, it’s 50%. If I say that they’re applying for full forgiveness and something is not adding up, I’m going to reach out to them and say, help me through the numbers because I’m not getting the same information. And then we kind of figure it out from there.

Charlie Venus (11m 31s):

As we sit here today, you know, we are dealing with is Delta variant of COVID-19 and potentially could have in economic input so I’m going to ask you to put your crystal ball

Jenny Shtipelman (11m 44s):

Turn on my crystal ball? And today’s the day where I left it at home. Come on. It, it should have been on the podcast prep was “bring your crystal ball”

Charlie Venus (11m 52s):

And do you see anything changing?

Jenny Shtipelman (11m 55s):

So we’ll see. I don’t know. I honestly couldn’t even tell you. If there is another iteration of this program, great. We’re happy to help our borrowers and the community. What the government will actually do? Who knows, whether we are going to be potentially go back to a full shutdown or maybe we’ll just go back to wearing masks or, you know, what is, what’s gonna happen? We’ll see.

Charlie Venus (12m 19s):

Yeah, because I was just curious if they might have any, you know, just an extension of the loan forgiveness period, time will tell, you know, if we do have any significant economic impact.

Jenny Shtipelman (12m 28s):

So forgiveness is not going to be as impacted as potentially just maybe a new program. Because again, from the time that people have gotten funding from their loan, they only have between eight and 24 weeks to spend the funds. And so they shouldn’t be spending those monies as we speak now. Right. And so if there’s any type of effect by the Delta variant in terms of its type of restrictions or, or anything else, we’re not, we’re not seeing it yet. Maybe when the weather will change, who knows, at that point, the government is going to have to figure out how are they going to proceed. But for now the funds that people have received should have been spent on those authorized expenses.

Jenny Shtipelman (13m 14s):

And so if they needed more money, that would be more money, but not the same money.

Charlie Venus (13m 19s):

Any additional parting information that you would want to share with the audience about PPP Loan, Forgiveness,

Jenny Shtipelman (13m 26s):

Document, document, document. So definitely keep all of the supporting documents. By law, you have to keep everything for six years. So even if you get full forgiveness and everything is good to go, keep it because the government has a right to go and audit whatever they want whenever they want. And just be proactive and reach out to your bankers and ask questions if you have them. Involve your CPAs and your attorneys if you had any concerns, because of the end of the day, bankers can not tell you how to run your business. We can help guide based on current law and what we’re seeing in our policy, but some of those business decisions, you know, that you would have to make, and if you’re not sure, then involve some other professionals that can help.

Charlie Venus (14m 7s):

Thank you very much, Jenny. This has been very enlightening.

Jenny Shtipelman (14m 11s):

Absolutely. My pleasure. My pleasure. I’ve been swimming in this pond for however many months it’s been going on. So happy to help.

Edwin K. Morris (14m 18s):

Thanks for listening to this edition of Charlie’s corner brought to you by Iroquois Group. I am Edwin K. Morris, and I invite you to join us for the next edition of the Trusted Advisor podcast.