Part 2 is here! If you missed the first episode in this mini-series be sure to go back and listen as Charlie Venus explores 3 key Specialty Lines with Jackie LaRock, Executive VP at RT Specialty. In this episode, Jackie discusses the ongoing hardening of the market for D&O, especially for public D&O. Jackie explains the three components of a D&O policy and how COVID-19 and other factors have affected the marketplace.

Edwin K. Morris (7s):

Welcome to the trusted advisor podcast brought to you by Iroquois group. Iroquois is your trusted advisor in all things insurance. This week, you’re listening to Charlie’s corner, a segment hosted by our very own Charlie Venus.

Charlie Venus (22s):

Welcome back, Jackie LaRock of RT Specialty, last time we signed off after covering cyber liability, we are excited to dive into D&O today. So what, what are the market trends there? What’s going on from a claim standpoint? And what do you see the impact of COVID-19 on the D&O marketplace?

Jackie LaRock (41s):

So the public D&O marketplace is in a very difficult spot right now. It has been hardening for years due to difficulties with claims activity and premiums being below where they needed to be. So the, the carriers have been looking for a rate for the last year or two years, depending on the risk. On top of that, we’ve had very low investment returns. Carriers looking for their investment returns to help buoy their overall financials. They have not been successful in that area. On top of this, we’ve had social inflation and we’ve had event driven litigation. So think of like me too type situations that have caused an increase in claims. With COVID, losses have continued to rise, and the underwriters have been worried about the typical exposures you have when you’re in a financial, financially difficult economy.

Jackie LaRock (1m 34s):

Those include financial insolvency, poor management, reductions in personnel, and then additional exposures that quite frankly might have may not have all surfaced yet at the present time. Underwriters have shared that they have, they in the past were asked to underwrite accounts, by looking at the financials. Now they’re being asked to look at accounts from the perspective of who can survive the pandemic. So in the past, it was common to see changes in rates, retentions, and limits. The typically didn’t see all three variables impacted at the same time, but since mid April of this year to the present, we are seeing changes in all those attributes.

Jackie LaRock (2m 14s):

So rates are going up, retentions are going up and limits are going down. Capacities and marketplace has diminished with many markets either pulling back or even exiting public D&O. And this worldwide has had a dramatic impact on the availability of public D&O insurance, with this impact being felt in London, Australia, obviously the U S. There is new capacity coming to the marketplace, but it’s not quite there yet. The impact to coverage has been a fairly significant, so the enhancements that have been added over the years are being peeled back. Most policies are currently offering narrow coverage, some offering significantly narrow coverage, and on top of it, the insured they’re facing sticker shock as they have come up on the renewals.

Charlie Venus (2m 59s):

Could you give a, like a quick overview of side A coverage, side B coverage, and side C coverage for the listeners?

Jackie LaRock (3m 9s):

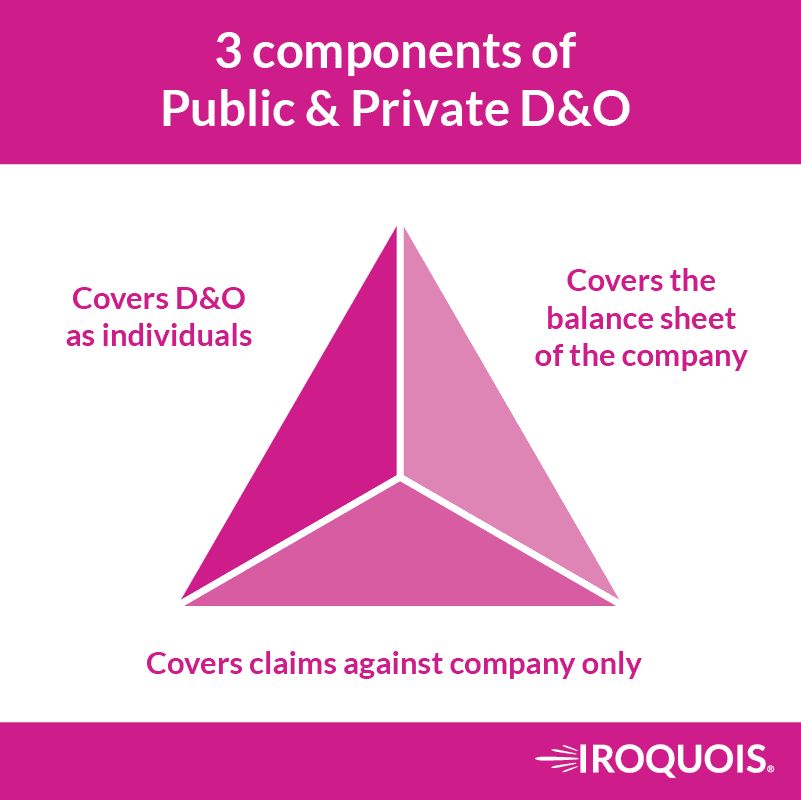

Absolutely. So D&O insurance is comprised of three insuring agreements, and they’re commonly referred to as sides A, B and C. Side A coverage protects the directors and officers as individuals and a response in the event that the entity is unable to indemnify the directors and officers. So this coverage typically responds when the insured is financially insolvent. So side A coverage responds when the entity is unable to indemnify directors and officers, or where there is a settlement or judgment connection with a, with a derivative action. So side A coverage is referred to as sleep insurance for directors and officers, because again, it’s there to protect them and respond without any retention.

Jackie LaRock (3m 51s):

Side B coverage protects the balance sheet of the insured entity by indemnifying the directors and officers when claims are made against them. So this is the coverage response when the entity can indemnify the directors and officers, but again it protects the balance sheet of the insured entity. Side C coverage protects the balance sheet of the injured entity, but it’s limited to claims against the entity. So with public accounts, side C coverage is limited to securities claims, meaning allegations of violations of securities laws. For private insurance, private company insurance, side C coverage is much broader and is not limited to security.

Charlie Venus (4m 27s):

Thanks. I really appreciate that. And so you had given the overview on public D&O. Is private D&O seeing the same issues from a rate standpoint reductions in coverages?

Jackie LaRock (4m 41s):

Yes. Private D&O has followed the path of public D&O, but it has not been as severe in terms of the market correction, if you will. So underwriters have recalibrated their underwriting. They are also looking to reduce their limits. So that is fairly common as well. Retentions are increasing. And again, these, these factors are being more aggressively addressed in midsize to larger private companies, but it is impacting nearly all sectors for private D&O insurance.

Charlie Venus (5m 17s):

Oh, from a rate perspective, what are you typically seeing on a private D&O – somewhere in the 15 to 25% range?

Jackie LaRock (5m 26s):

It can be that range, or it can be significantly higher as high as reducing the limit in half and the premium staying the same. So it can be very difficult for insureds that perhaps were not in the most strong position financially, previously. And so now their terms are looking at very, very differently from where they were in the past. And then additionally, the rates for certain companies, certain sectors that are viewed as more difficult for underwriters had been more aggressively impacted by underwriters in terms of rates.

Charlie Venus (5m 59s):

Now a lot of those industries is that because of COVID or a combination of COVID and other factors?

Jackie LaRock (6m 6s):

It’s a combination of COVID and the current economic climate that we’re in caused by COVID. So there are some concerns about COVID exposures, but again, the financial impact that it’s had to both operations and revenues and overall financial wherewithal of companies is really what’s driving the underwriting changes

Charlie Venus (6m 29s):

What kind of claims are being seen in private and public D&O from, as a result of COVID. I mean, I know that there’s, you know, there’s issues from a safety standpoint, from a liability standpoint, a financial standpoint of the company, if they didn’t act responsibly. So what’s, what, what are you seeing there

Jackie LaRock (6m 52s):

In terms of the claims, as you mentioned, it’s very common to see more claims relating to the financial condition of the company, so that those are the types of claims that you see in any economic downturn. The difference now is that there are additional government programs such as the cares act, the payment protection program, otherwise known as PPE, which have impacted underwriting because those programs have specific requirements as respect certifications by applicants for seeking a loan and also seeking forgiveness of those loans. So those are causing additional exposures for D&O underwriters.

Jackie LaRock (7m 35s):

And I personally have seen carriers adding exclusions on because they did not want to pick up that exposure. There are particular policies, specific policies, I should say, in the marketplace that address the PPP and the cares act type exposures. That again, tend to, can be underwritten for insureds to deal with their, their exposure to certification type issues, and also application of the funds in an appropriate matter, in compliance with those programs. So the false claims act again, is the crux of where this exposure is. And, and briefly to explain the false claims act allows for that proceeding to be brought against a company that is, makes misrepresentations in connection with funding from the government.

Jackie LaRock (8m 25s):

So obviously these loans are funds from the federal government. So there are requirements to comply with appropriate certifications, to the extent that there’s a determination that a company may not have applied to those certifications that creates liability under the false claims act. There are penalties that can be assessed, damages that can be assessed. And on top of that, there are whistleblower claims that can be filed under the FCA that can be expensive to defend and difficult to deal with from a media standpoint as well.

Charlie Venus (8m 58s):

Jackie, we hear a lot about social inflation in the auto market and the umbrella market as well. Is that an impact in the D&O and EPL markets too?

Jackie LaRock (9m 9s):

Absolutely. So along with the low interest rate return that I mentioned early on, the impact of social inflation, that is the cost of settling claims that concerns about judgment, et cetera, has certainly increased the losses and that correspondingly is impacting the premiums and the retentions on the D&O book.

Charlie Venus (9m 32s):

So just adding to what’s already going on in all the other lines of business. What do carriers that you deal with, what do they suggest to boards of directors and the executives to protect themselves and their companies? Are there any, anything that they’re pushing out there in terms of this is what you need to be doing in this really dire time to protect your company?

Jackie LaRock (9m 59s):

I think this is an important topic, Charlie, and I appreciate you raising it. So board members have fiduciary obligations of care and loyalty, and that means they need to act in the best interest of the company for which they serve. Looking at the exposures that companies have in the current environment. I viewed the duty of care as being translated into obligations as oversight and disclosure. That’s what underwriting are liberally looking to see how companies are handling these exposures. So to the extent that directors and officers are aware and taking appropriate steps and have appropriate oversight of various exposures, and that is viewed as a positive factor. So oversight in the context of ensuring safety protocols are in place and being solid to protect employees, customers, et cetera, oversight financially, as respect to understanding the impact of the pandemic and making appropriate disclosures.

Jackie LaRock (10m 52s):

Certainly if you’re a public company, you have to make appropriate disclosures, but also again, understanding the financial impact in the private company sector as well. We already mentioned oversight as respects government funds and loans. And here again, the focus is ensuring that someone is checking the accuracy of the certifications for loan applications and forgiveness applications, as well as having some oversight to make sure that governmental funds are being used for the purpose for which they were intended. The goal is to avoid media publicity regarding wrongdoing as that exposure can certainly result in a higher potential for claims.

Charlie Venus (11m 27s):

Wow. That great response. Yeah. Thanks again, Jackie, for the rundown on D&O, we’ll be back in the studio soon to cover EPL and market trends.

Edwin K. Morris (11m 36s):

Thanks for listening to this edition of Charlie’s corner brought to you by Iroquois. I am Edwin K. Morris, and I invite you to join us for the next edition of the trusted advisor podcast.