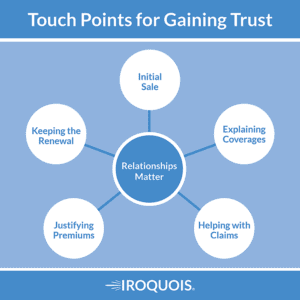

Join agency owner Aaron Benton. Firstly, Aaron tells The Trusted Advisor why relationships, which are often seen as the way into selling a new large account, are just as critical to maintaining that account. Aaron, in his laid-back conversational style, shares several real-life experiences. Experiences that brought this point home to him as he looked to grow his agency by writing middle market accounts. In conclusion, relationships matter. For more podcasts like this one click here.

Edwin K. Morris (4s):

Welcome to the trusted advisor podcast brought to you by Iroquois group. Iroquois is your trusted advisor in all things insurance. I am Edwin K. Morris. We’re speaking today with Aaron Benton. He is the chief sales officer of the Genesee Valley agency and is a graduate of SUNY Cobleskill, earning a bachelor’s degree with a financial services major. Prior to that, he worked in an underwriting support position at Sterling insurance company in Cobleskill, New York. How does middle markets even work as an industry segment? What is it and how do you approach?

Aaron Benton (41s):

I guess, you know, just a start is to what is middle market? And, you know, you could ask that question to several different people, carrier agent, marketing reps, whatever, and they’re all going to give you a different answer. Generally, when I think of middle markets, it’s a premium level. Some companies consider it 20, maybe 50 or a hundred thousand in total package premium, but really, you know, I think complexity of it is a good starting point too. This isn’t, you know, for any business. When I think about like run of the mill business, I can quote it online. I can get it, get it done in 15, 20 minutes. When it comes to these complex middle market accounts, I’m sitting at the office analyzing what their exposures are and then thinking, well, this is what their exposure is now, where am I going to go with it?

Aaron Benton (1m 27s):

And it’s not something that can typically just be entered into the computer. Sometimes it is, but not generally. So I’m filling out a court applications that can be cumbersome. There’s a lot of, a lot of information, a lot of data that goes into that. And it’s imperative that that information and data is accurate so what I get as a proposal on the, on the end of it, it is certainly accurate. So when I propose it to the insured or the client, prospect, whatever, we’re squared away, and we’re not going to have any issues upon binding. So, you know, if you want to talk about like a premium amount, maybe like 20,000, 20,000 would be a good starting point for middle market. And, you know, once you get it up into that level of premium, where there’s several thousand dollars of commission on the line, every agent within a hundred mile radius is trying to pursue that business and that, that brings a whole new level of anxiety, just aside from the fact that this is a big account that you can’t screw up or else it’s going to put your name on the line.

Aaron Benton (2m 20s):

It, there’s a lot of work that goes into retaining those accounts as well.

Edwin K. Morris (2m 24s):

How does one get into this? Did you start off in middle markets?

Aaron Benton (2m 29s):

No. So naturally it’s one of those things that you work up to in life. Just like a lot of things that you grow into. So in the beginning of my career, I started as a personal lines underwriter about 10 years ago, when I was 21 years old, fresh out of college, just got my internship done. I started as a personal lines underwriter, grew into some drawing fire, landlord, lessors risk type underwriting, marketing rep. And then I had the opportunity to come back to my hometown to advance my career. So getting into your specific questions, how did I get into middle market. Well now being a producer, I had no experience as to this type of business being on the company side of things. When I came back to the agency, naturally the goal here is to grow.

Aaron Benton (3m 17s):

We’re salespeople, you know, so selling $500,000 policies just wasn’t going to work out. You know, we have to get up into the several thousand dollar mark in order to be as efficient and as effective as possible, looking and prospecting those specific clients. They’re going to add numbers to your bottom line. Yeah, it’s more complex, but in that complexity, it gets more exciting, you know, and I feel that excitement, you know, there are certain accounts that are a thousand, 2000 bucks. It’s like, man, do I want to put my effort into that? You start talking 20, 30, 40, 50 grand. You really get pumped up to write that business.

Edwin K. Morris (3m 46s):

So we’ve talked about the why, why you get there? Why, what drove that decision point for you to develop your skillset, to get into this? Can you give us a, an idea of what, what it looks like when the rubber hits the road? I mean, the selling is, that is the easy part, right? To some degree, because now you’ve got to continue that relationship. Maybe they’ll shop you against somebody else. And you know, so it’s a constant engagement, but what’s it look like when something happens? Do you have any examples?

Aaron Benton (4m 16s):

The way they fall into place is, in almost every case, is different. I mean, I’ve gone out and gotten accounts simply by knocking on their door. I know what I’m looking for. Like one thing I like to personally write is garage business, a garage liability policy. So I, I kind of prospect on online while I think I, you know, I think that would be a good fit for the markets in which I have in my office. So then I figure out who owns it. I go up to their Facebook, the County website, look at the tax records, figure out who owns it. And then I show up at their front door and say, Hey, I’m Arron Benton from Genesee Valley agency. Can I look at your insurance? You know, have you shopped it out in a few years? You know, I’m here for a reason. I wouldn’t be here wasting my time. And certainly not yours. Give us an opportunity.

Aaron Benton (4m 56s):

I can show you what we can do. That’s one way. I have also, and we’ll get into it later, you know, in my extracurricular activities, being outside the office, whether it’s skeet shooting, hanging out at the gun club, social clubs, those people become your friends and trusted, you know, just trusted acquaintances. So a few months ago, I was at the, at the gun club shooting some practice with some friends. And there was an older gentleman there that wanted to tag along with us, fine, whatever I’m okay to help people where I can. Come to find out he’s an executive at this pharmaceutical company. You know, I got to know him. And several months later we got talking about their insurance and I’m going to have an opportunity to quote that. So it really depends.

Aaron Benton (5m 36s):

And you know, things just fall into place, whether it comes from extracurricular or square peg square hole – type marketing, knocking on their front door, it, it comes from multiple different directions,

Edwin K. Morris (5m 47s):

We’ve talked about the selling of the product, but what happens at the other end of that cycle when somebody needs help?

Aaron Benton (5m 54s):

So, you know, upfront, we’re doing our competitive shopping, doing our, our, our rate, getting things going, but there there’s an expectation on the back end of that, when there’s an issue, you know, currently we have a municipality $20,000 range for its premium. They had a large fire yesterday and, you know, naturally they expect us as their agent to go out and offer that moral support. Whether it’s getting, you know, the restoration crews out there, getting the adjusters online, talking to them about what coverages they have to ease their mind. Because naturally you have in this particular case, it’s going to be well over a million dollar claim. They’re worried, their first worry is, do we have enough insurance? The first issue that comes to mind.

Aaron Benton (6m 34s):

So I try to go out there, you know, let them talk to me, let that anxiety flow out of their body because they’re certainly just worked up, hear them out, talk to them about what they have, let them know that things are going to take some time, but it’s all going to be fine. If we’re doing our job on the backend, offering the right coverages, not skipping where we shouldn’t be. Things will play out. Yeah. Nobody wants to go through these significant losses, but it happens. That’s the whole point of insurance. So being there on the backend, offering that moral support, getting the certain vendors, adjusters, restoration crews out there and help them where we can and then pass it off to the company in a seamless manner is, is the time to endear ourselves to our clients.

Aaron Benton (7m 15s):

And what helps that account stick within our office gives, it a less chance to leave our office.

Edwin K. Morris (7m 20s):

That relationship is constructed almost like, I’m hearing what you’re saying, so it’s almost like a first responder. And if you’re part of that first response, you’re the face, right? You’re the connection. And if you can help provide solutions, keep the wheels moving forward and absorb some of that anxiety, then they’ve got a friend. Yeah.

Aaron Benton (7m 37s):

And you know, it, I’m never going to have a claim. That’s what we hear all the time. It’s never going to happen to us until it does. And then so in this industry, a lot of it has to do with price. With that price shopping, things get left out. Insurance costs a dollar, whether it’s a dollar here or a dollar here, Company A or B, how they do it, it’s eventually going to catch up to them. So how can we offer them the most comprehensive package at the most competitive rate for the exposure in which they have, if we do what we, what we do best and do the right thing on the backend, things will fall into place. That client customer is going to tell people about us. They’re going to stick with us because they had a good experience. And that is paramount to what we do.

Edwin K. Morris (8m 15s):

That’s kinda like the, the, the coverage of an automobile, you know? So it’s like, well, it’s not financed anymore. We don’t need full coverage. So, you know, and then it’s like, Oh no…

Aaron Benton (8m 25s):

Yeah. Until you’d have to come out of pocket 10, 20 grand. In this particular case, I guess, to compare this to a, an example that happened, it wasn’t in our office, a year ago, the local County from my understanding has a lot of their property coverage what they would consider self-insured, they’re not going to self-insure their liability, but they’re going to self-insure their property in order to limit the insurance perspective. Well, one of these buildings burnt down and now they’re left, which I I’m certain that it was a million dollar claim that they’re going to be paying out of pocket for. Who really wants to do that? But it doesn’t, you know, it doesn’t really hit home until you go through it yourself.

Edwin K. Morris (8m 59s):

Penny-wise, dollar foolish. Well, Aaron, thank you very much for educating us on middle markets and hopefully your customer will have a quick turnaround in their claim.

Aaron Benton (9m 8s):

Certainly.

Edwin K. Morris (9m 13s):

Thanks for listening to this edition of the trusted advisor podcast brought to you by Iroquois group. Iroquois, your trusted advisor for all things insurance, and remember get out of the office and sell. this program was recorded live at the Cohen multimedia studio on the grounds of Chautauqua institution. I am Edwin K. Morris, and I invite you to join me for the next edition of the trusted advisor podcast.